Comparing Supplement Plans with Original Medicare and Part C

Medicare Supplement Plans, also referred to as Medigap, are not stand-alone Medicare Plans. They fill in the gaps in the Original Medicare Plan where the plan’s coverage stops. These plans are provided by private insurance companies, but they are approved by Medicare.

Original Medicare and Medigap

Original Medicare is composed of two of the four parts of Medicare: Part A and Part B. Medicare Part A is considered “hospital insurance,” while Medicare Part B is considered more along the lines of actual “health insurance,” since it covers sick visits and preventative services.

Once you enroll in the Original Medicare Plan, you’re eligible to enroll in a Medicare Supplement Plan or Medigap. Enrolling in one of these supplement plans does not replace your Original Medicare Plan — it simply helps reduce your out-of-pocket costs that are caused by what is not covered under Original Medicare.

Medigap assists with deductibles, copayments, and coinsurance costs. Some of the Medigap plans that are offered also offer coverage for things that Original Medicare would not, such as medical care when traveling outside the United States.

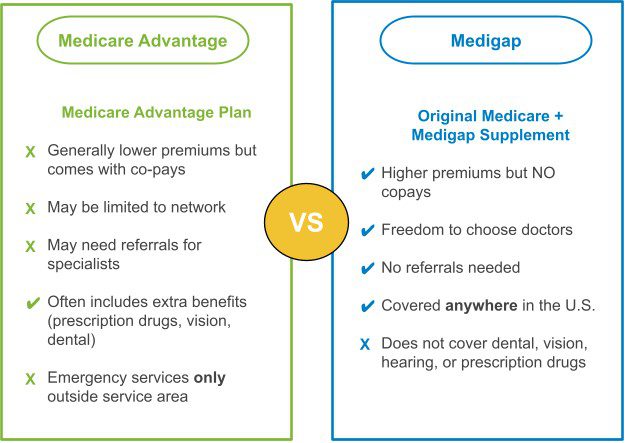

Medicare Advantage and Medigap

You cannot be enrolled in a Medicare Advantage Plan and a Medigap Plan at the same time. You’re only eligible for a Medigap Plan if you have both Parts A and B. Medicare Advantage Plans, also known as Medicare Part C, provide and usually exceed the benefits offered by Original Medicare.

Medigap fills in for Original Medicare; Medicare Advantage Plans not only provide hospital and medical coverage, but they also typically offer prescription drug coverage, as well as vision, dental, and hearing benefits. Some even offer transportation to and from the doctor and a free or discounted gym membership.

One advantage of being enrolled in Original Medicare and a Medicare Supplement Plan, though, is that you’re eligible to receive treatment anywhere across the United States, as long as they accept Medicare. When enrolled in a Medicare Advantage Plan, you typically enroll in either an HMO (Health Maintenance Organization plan) or a PPO (Preferred Provider Organization plan).

HMOs and PPOs have in-network providers that they prefer you to choose from. If you decide to seek out-of-network treatment, then you’ll pay more out-of-pocket, and may not receive any aid from your Medicare Advantage Plan at all. However, a PPO plan is a bit more lenient than HMO.

Important Facts To Know About Medigap Policies

Remember, in order to enroll in a Medicare Supplement Plan, you must first enroll in Medicare Parts A and B, aka Original Medicare. Medicare Supplement Plans and Medicare Advantage Plans are not the same types of plans.

- Medigap helps fill the gaps to ease your out-of-pocket costs.

- Medicare Advantage Plans actually provide full health insurance coverage once enrolled.

You may also be required to pay a monthly premium for your Medigap Plan. If so, you’re still responsible for paying the Medicare Part B monthly premium as well. As of 2006, Medigap plans cannot cover prescription medications, so you must purchase a separate Medicare Part D drug coverage plan. You’re also responsible for that premium, although some people qualify for the Extra Help program.

Want to Learn More? Reach Out Today

At iHealthcare, we care about providing you with as much information as possible about your Medicare options. If you’re interested in a Medicare Supplement Plan and would like to learn more about the coverage involved with a Medicare Supplement, give us a call today. We’re here to help!